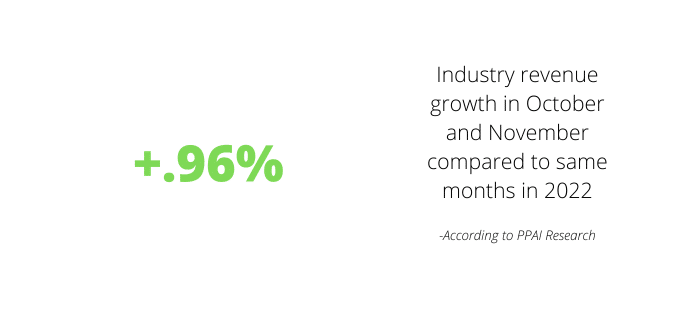

Promotional products industry revenue had only modest growth in October and November, growing at a rate of only 0.96% compared to the same months in 2022.

- This makes October and November the slowest two-month period of the year so far, according to PPAI, just after August and September had produced the slowest month up to that point at 1.3% revenue growth.

- This growth is being noticeably outpaced by the annual rate of inflation, which was 3.2% for the end of November, according to the U.S. Bureau of Labor Statistics, though it has also begun to level over the past several months.

- The latest revenue data isn’t cultivated from the same methodology as the annual Distributor Sales Volume Estimate, which polls distributors of all sizes. Rather, the current assessment is discerned from the aggregated results of PPAI 100 suppliers responding to a flash survey.

Alok Bhat, market economist and senior manager of research at PPAI, has noted a number of factors that distributors and suppliers are attributing this minor growth to. Continued economic uncertainty is becoming an even more significant concern among promo companies in Q4 while price competition and long sales cycles remain business challenges for many.

“This shift [from 1.3% growth in August and September to 0.96% growth in October and November] underscores the importance of strategic agility to enhance growth and market competitiveness,” says Bhat.

Bhat also notes “market optimism” and “industry resilience” when looking at the order volume reported by suppliers, as well as a blend of “growth, stability and decline among distributors,” which he says calls for “agile, adaptive strategies to meet evolving trends and consumer needs.”

Supplier Challenges

In the previous bi-monthly sales report, 82% of participating PPAI 100 suppliers cited economic uncertainty as the most significant challenge facing their business.

- If that number seemed high at the time, it only increased over the following two months.

- In October and November, 91% of respondents claimed economic uncertainty presented a challenge to business.

- Indeed, nearly all participating suppliers feeling they have to tip-toe around the economy reflects a heightened sense of unpredictability and risk in the market.

In early August, PPAI Media published a special report on the divided outlook among promo professionals concerning the state of the economy, which touched on what one economist called “the recession that refused to be.” As predicted by that economist, a recession has still not technically manifested, but this recent survey suggests that the general uncertainty has still managed to make life difficult throughout the industry.

The next two most pressing challenges facing suppliers, according to the survey, remain the same as the previous bi-monthly report, but the two are trending in opposite directions.

- Price competition is a concern for 35% of respondents, which is down from 41% in August/September.

This may suggest a stabilization in the market’s competitive pricing dynamics or a change in competitive strategies among suppliers. The chief operating officer at one PPAI 100 apparel supplier offers up a prediction for price competition going into 2024.

“Most suppliers will likely hold ground on price increases, and I expect many to offer sales/promotions to help move overstocked inventory in 2024,” the COO says. “It’s a deal-oriented environment if the business environment gets tougher with slower growth. It’s tricky, as overseas suppliers are still experiencing inflation and rising labor costs, although freight costs have dramatically dropped. Cotton prices, for example, are still challenging with China restrictions and bans due to supply.”

- Meanwhile, there has been a notable increase in concerns about lengthy sales cycles over the last two months from 36% in August/September to 44% in October and November.

This trend could indicate an increasing complexity in sales processes or heightened competition leading to more prolonged decision-making by clients.

A point of improvement over the course of October and November is the significant decrease of suppliers who reported challenges with managing customer expectation.

- Back in August and September, 22% of respondents saw customer expectations as a challenge compared to only 9% in October/November.

Supply chain challenges remain to be a problem for a small but consistent number of suppliers. Difficulties navigating the supply chain were reported by 13% of respondents compared to 14% in the previous two months.

Distributor Challenges

There is an even greater jump in concern over economic uncertainty on the distributor side of things. In fact, the number jumps right off the page.

- A staggering 94% of participating distributors are now claiming economic uncertainty as a critical challenge.

- This number is up by nearly a third from the previous bi-monthly report which cited 67% as sharing that concern.

Amy Spychalla, VP, strategic operations at American Solutions for Business, says it is not necessarily one big inciting event – such as a recession that is causing uncertainty but businesses and consumers juggling so many different potential future outcomes or obstacles.

“There’s a lot going on in the world today, and we’re all trying to peek around the corner to see what lies ahead,” says Spychalla.

Similarly, long sales cycles are a challenge for a growing number of distributor respondents.

- 44% of distributors, up from 33%, are citing sales cycles longer than they would normally expect or hope for.

Spychalla sees this as a somewhat unavoidable part of business that requires proper reaction.

“We love having projects in every stage of the pipeline as some deals do take longer,” Spychalla says. “Customer contacts are wearing multiple hats and there’s a lot of change going on within organizations, which can cause delays. Patience and continual follow-up are key.”

- Price competition and managing customer expectations is a challenge for one third of responding distributors, with customer expectation concerns being up from 28% in August and September.

Interestingly, distributors – who are somewhat removed from the supply chain compared to suppliers but still affected by the outcome of disruptions – did not prominently cite the supply chain as a current challenge. This is an improvement from the previous bi-monthly report, in which 7% of the responding distributors noted disruptions caused by supply chain.